The Post-COVID Economy

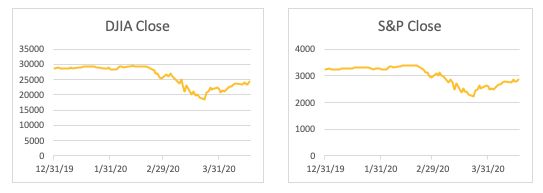

In addition to the health and human suffering resulting from the coronavirus (“COVID-19”), the economic impacts on the economy and financial markets have been staggering. The Dow Jones Industrial Average (“DJIA”) and S&P 500 both reached record highs in February 2020 with the Dow soaring to 29,551 on February 12, 2020, and the S&P reaching its high of 3,386 on February 19, 2020. Since these peaks, the financial markets have crashed with both indexes declining more than a third by March 23, 2020. By the market close on Friday, April 17, 2020, both the DJIA and S&P 500 had recovered more than half of the recent decline.

While the financial markets have been severely impacted, the overall economy is far more worrisome with 22 million Americans filing unemployment claims since mid-March and millions of Americans being furloughed. More than previous economic collapses, small businesses and the American consumer have been particularly hard hit by the intertwining personal health and financial crises emanating from COVID-19.

The current American economy is primarily consumer-driven, representing 68% of overall GDP in the fourth quarter of 2019. Many of these consumers are employed in small businesses and the spread of COVID-19 is having a devastating impact on their full-time employees and hourly workers whose hours, shifts, and operations are coming to a full stop.

Over 99 percent of America’s 28.7 million firms are small businesses. They create two-thirds of new jobs and drive competitiveness and innovation. A study conducted by the Small Business Administration (“SBA”) found that small businesses produce 16 times more patents per employee compared to larger patenting firms. The vast majority (88 percent) of employer firms have fewer than 20 employees, and nearly 40 percent of all enterprises have under $100,000 in revenue.

These are businesses that comprise the soul of America and are the fabric of our communities. They include restaurants, retail, business services, health and fitness, automotive repair, in-home care, technology, travel and lodging, movie theaters, and sports and recreation. Forced closures of these enterprises coupled with shelter in-home policies have brought more than half of small businesses to a stop. The monthly loss per employee exceeds $1,500 and results in a US-wide income loss per month ranging between $70 billion to $80 billion. Hourly workers in urban environments have been especially hard hit as Boston, Las Vegas, New York, Pittsburgh, San Francisco, and San Jose had reductions in hours worked of greater than 50%. In New York City, the epicenter of the pandemic, hourly workers have seen their hours decline by 75%.

To address the COVID-19 pandemic, Congress passed, and the President signed in late March 2020, the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”). It provides $2.2 trillion to help households, small businesses, state and local governments, and corporations to weather the crisis. In addition, stimulus programs by the Federal Reserve have pumped about $1.6 trillion into financial markets in the past month, and the total could reach $2 trillion—or 10% of U.S. GDP.

A significant component of the CARES act for small business is the Payroll Protection Program (“PPP”), which was funded at $349 billion. This program is available for any small business with less than 500 employees, including sole proprietorships, independent contractors, and self-employed persons, as well as non-profit organizations, and is separate and distinct from the Economic Injury Disaster Loan (“EIDL”). The PPP is a loan designed to provide a direct incentive for small businesses to keep their workers on payroll. The SBA will forgive loans if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.

Unfortunately, the need is much deeper than the initial stimulus funding contemplated, and in less than two weeks, by April 16, 2020, the PPP had run out of money. As of this writing, lawmakers on Capitol Hill are finalizing measures to expand the funding for this program by $310 billion.

There are some other options for small businesses to consider; however, each comes with a cost. The employee-retention tax credit was recently introduced as part of the CARES Act as an alternative incentive to encourage employers to keep workers on payroll. The credit equates to 50% of employee wages paid by an eligible employer in a 2020 calendar quarter and the credit is subject to an overall wage cap of $10,000 per eligible employee. However, if you take advantage of the credit, you cannot qualify for PPP and vice versa.

Venture-Capital funding is another potential funding source. While entities that receive venture-capital financing are not typically responsible for paying it back, they often must forfeit a portion of their control of the business.

Crowdfunding is a form of crowdsourcing and is an alternative financing option. The project or venture is funded by raising small amounts of money from a large number of people, typically via the Internet.

While these funding programs are helpful, the best antidote to alleviate the economic collapse is for the economy to reopen. To date, there has not been a united consensus, either domestically or internationally, on how or when this should happen, or what the new normal will look like. Pending a vaccine or treatment, the issue will continue to be debated and decisions questioned.

Arguments have been raised pitting economic losses against health concerns resulting in a debate as to whether the pandemic cure – and the components of social distancing, closed businesses, rising unemployment, increasing federal deficits, and a potential total economic collapse – is worse than the disease itself. Lockdowns clearly have health benefits as fewer people will die of COVID-19, as well as other transmissible diseases. But they also have real social and economic costs including social isolation, mental and physical health concerns, unemployment, and widespread bankruptcies. Moving forward, we need to compare the impact different policies have on the overall well-being of our population.

The issue appears to be moving in the direction of a gradual reopening of the economy in stages and in regions that have been the least impacted. Great care will be given to monitoring the impact of these openings. Increases in new cases will lead state and local leaders to pause and to move even more deliberately.

Greater testing needs to occur to have people safely return to work, school, and leisure time activities. Complicating the effort to increase the number of tests performed in the United States is a shortage of equipment needed to conduct the screenings. According to the Center for Disease Control and Prevention (“CDC”), there are roughly 120,000 samples tested each day. Many experts believe that the number of daily tests performed will have to increase into the millions in order to safely reopen the economy. Optimally this would be accompanied by a related program to trace people who have had contact with infected people in order to stop them from further spreading the coronavirus. Getting a sufficient level of testing and tracing is going to take a lot of effort and massive funding; however, failure to do so may lead to a second or third wave of COVID-19 infections that could kill more people than we have already seen, and lead to further shutdowns of businesses that ultimately end up doing greater economic damage than has already been experienced.

Going forward, we will see a different economy. This economic crisis is a combination of supply and demand shortages, and much of it is self-imposed by government action. While a strong recovery is theoretically possible as the government reactivates sections of the economy, a longer pandemic shutdown will likely lead to destroying jobs permanently as consumer purchasing power will have eroded.

Supply chains will certainly come under scrutiny. Changes to increase their flexibility and resilience through stronger and varied networks of suppliers are likely to increase the cost of business for manufacturing and construction companies. Business leaders need to prepare for the effects on production, transport and logistics, and customer demand.

Certain industries that were particularly hard hit, including aerospace, travel, and insurance, may see a slow recovery. Commercial real estate will be negatively impacted from non-payments by tenants, a slow return to office space as the virus lingers, and certain businesses that will allow employees to continue to work remotely from home.

For individuals, life will be irrevocably altered. Travel and entertainment will remain adversely impacted. Health professionals will continue to advise people to travel only if necessary, to lower their risk of catching the virus, and prevent the risk of spreading it. The continuation of social distancing will impact large social gatherings, including concerts and movie theaters, and restaurants will have to plan for a lower number of customers. The wearing of face masks, initially disregarded by the CDC, will be the new normal, and policies will be dictated by elected officials to ensure that people comply with wearing them.

The health and economic concerns raised by COVID-19 are daunting and require that our leaders and elected officials align to find effective policies and solutions. The year 2020 is also a Presidential election year. Political polarization and the continuance, or even increase, in a lack of bipartisanship will further undermine the US government’s response to the pandemic crisis. The COVID-19 pandemic is an enormous risk to all US citizens and our way of life. It is incumbent upon our leaders to act dutifully to defeat this threat.